The Basic Principles Of Kam Financial & Realty, Inc.

The Basic Principles Of Kam Financial & Realty, Inc.

Blog Article

Getting The Kam Financial & Realty, Inc. To Work

Table of ContentsKam Financial & Realty, Inc. Things To Know Before You BuyThe Ultimate Guide To Kam Financial & Realty, Inc.The Greatest Guide To Kam Financial & Realty, Inc.Some Ideas on Kam Financial & Realty, Inc. You Should Know5 Simple Techniques For Kam Financial & Realty, Inc.3 Simple Techniques For Kam Financial & Realty, Inc.

A home mortgage is a funding used to acquire or maintain a home, story of land, or various other actual estate.Home loan applications undertake a rigorous underwriting process before they reach the closing phase. Home loan types, such as standard or fixed-rate lendings, differ based upon the customer's requirements. Home mortgages are financings that are made use of to acquire homes and various other kinds of property. The residential property itself acts as collateral for the loan.

The price of a mortgage will rely on the kind of car loan, the term (such as thirty years), and the rates of interest that the lender charges. Home mortgage rates can vary widely depending on the sort of product and the certifications of the candidate. Zoe Hansen/ Investopedia Individuals and companies make use of home loans to acquire realty without paying the whole acquisition cost upfront.

Kam Financial & Realty, Inc. - The Facts

The majority of typical home loans are totally amortized. Common home mortgage terms are for 15 or 30 years.

A domestic property buyer pledges their residence to their lender, which then has a case on the building. In the situation of foreclosure, the lending institution might force out the locals, market the property, and use the cash from the sale to pay off the home mortgage financial debt.

The lending institution will certainly ask for evidence that the customer is qualified of repaying the funding. This might consist of bank and financial investment statements, current income tax return, and proof of current employment. The lender will normally run a credit scores check . If the application is accepted, the lender will certainly provide the borrower a finance of approximately a specific amount and at a certain rates of interest.

The 15-Second Trick For Kam Financial & Realty, Inc.

Being pre-approved for a home mortgage can give buyers an edge in a limited housing market since vendors will know that they have the money to support their deal. As soon as a customer and vendor concur on the terms of their deal, they or their representatives will fulfill at what's called a closing.

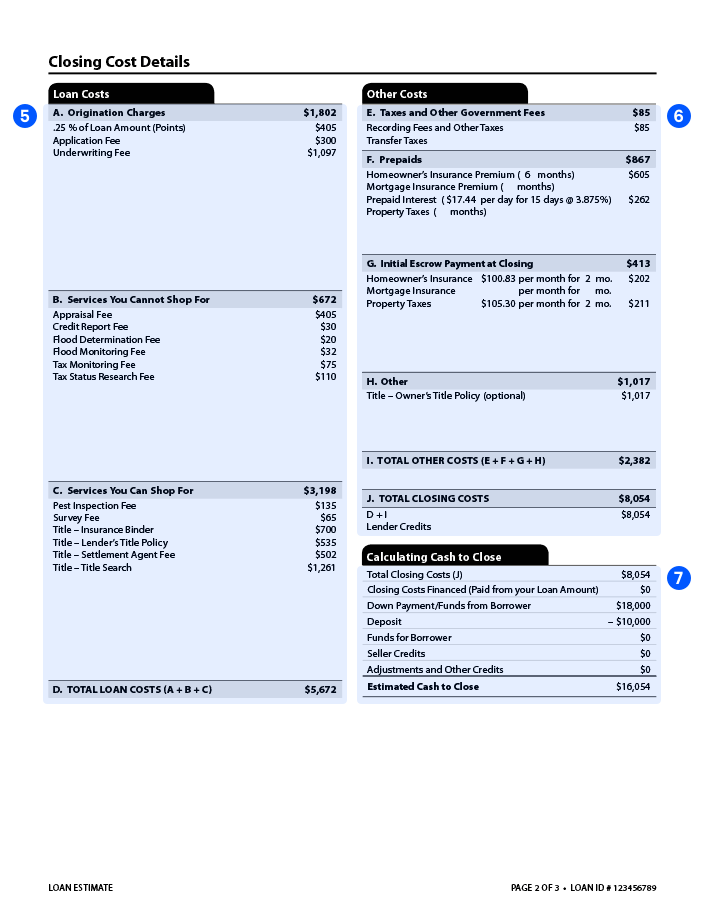

The seller will transfer ownership of the residential or commercial property to the buyer and get the agreed-upon amount of cash, and the purchaser will certainly sign any continuing to be mortgage records. The lender might charge fees for originating the lending (sometimes in the type of points) at the closing. There are numerous options on where you can obtain a home loan.

Getting My Kam Financial & Realty, Inc. To Work

The standard type of mortgage is fixed-rate. A fixed-rate home loan is additionally called a traditional mortgage.

Kam Financial & Realty, Inc. Fundamentals Explained

The whole financing balance comes to be due when the customer passes away, moves away permanently, or offers the home. Within each sort of home loan, debtors have the alternative to get price cut factors to buy their passion rate down. Points are basically a cost that consumers compensate front to have a lower interest price over the life of their car loan.

The Best Guide To Kam Financial & Realty, Inc.

Just how much you'll have to pay for a mortgage depends upon the kind (such as repaired or flexible), its term (such as 20 or thirty years), any kind of price cut points paid, and the rate of interest prices at the time. mortgage loan officer california. Rate of interest rates can differ from week to week and from lending institution to lender, so it pays to look around

If you default and confiscate on your home loan, nevertheless, the bank may come to be the brand-new proprietor of your home. The cost of a home is typically much above the amount of money that the majority of homes save. Therefore, mortgages allow individuals and households to acquire a home by putting down only a fairly little down payment, such as 20% of the acquisition price, and acquiring a car loan for the equilibrium.

Report this page